Summary

Highlights

We believe China’s tech sector offers attractive valuations and strong growth, making it a compelling diversification option.

Europe offers opportunities in AI-related capital goods, and small- to mid-cap companies focused on domestic markets.

A potential bottleneck in the tech transformation is energy, as AI and data-centre growth could increase electricity demand sharply.

In this edition

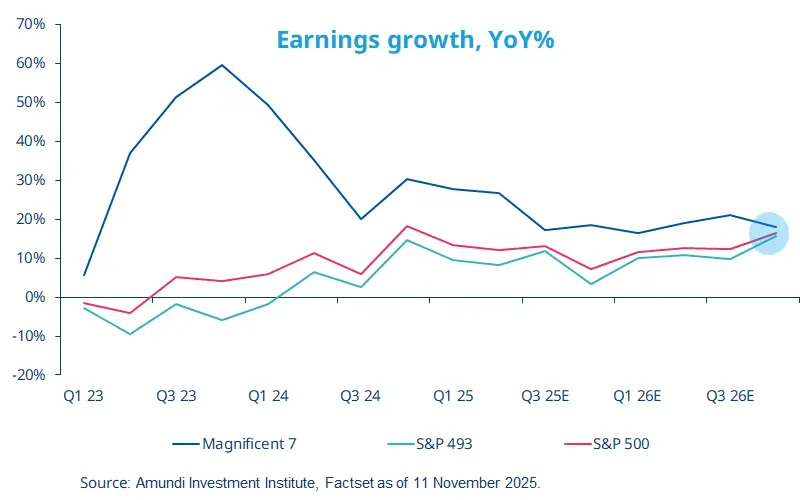

After reaching fresh all-time highs in October, global equity markets sold off early last week, particularly the US ‘Magnificent Seven’ group of stocks, driven by concerns about AI valuations. Good US earnings results have helped soothe market worries, but questions around the AI run remain. Over the past couple of years, earnings growth for the ‘Magnificent Seven’ stocks outpaced that of the remaining 493 stocks in the S&P 500 index by a wide margin, but this gap has narrowed recently and is expected to narrow further. As a result, earnings growth may converge across the US equity market. This, together with concentration risk in US mega-caps, argues for geographic and sector diversification away from the most expensive market segments and for exploration of other areas that are supported indirectly by AI capex, as we address in our just-released 2026 Investment outlook.

Key dates

Germany IFO business climate, Chicago Fed National Activity Index |

US GDP growth, US personal income and spending |

India GDP growth, France and Italy inflation rate |

Read more