Summary

Highlights

The latest IMF projections highlight that resilience to economic and geopolitical shocks has become a key variable for economic growth.

We think supply chains, energy independence, defence capabilities, infrastructure and access to critical raw materials will drive growth, inflation and asset allocation.

A consequence of these relationships is that policymaking will become difficult.

In this edition

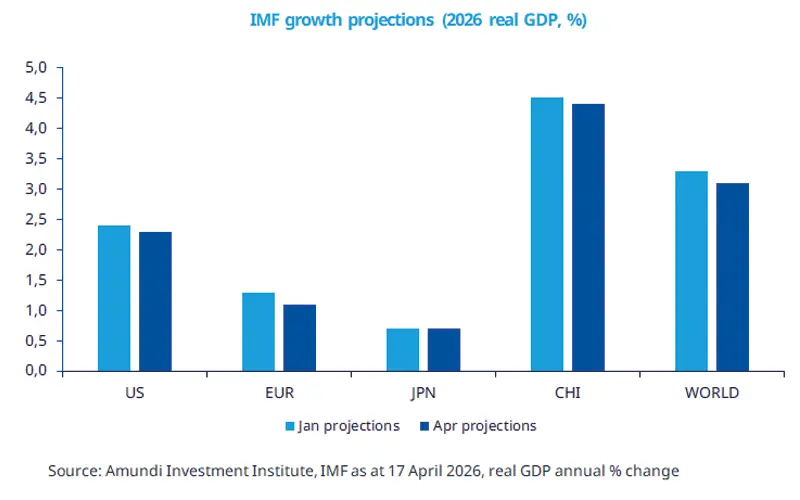

The IMF’s latest forecasts highlight that the global economy is still growing, but it has become more fragile. Before the recent conflict, economic growth was improving, whereas higher energy prices and greater uncertainty are now slowing that growth momentum.

For investors, the main point is no longer just weaker growth, but the risk that more expensive energy keeps inflation higher for longer and makes markets more volatile. The main themes to watch are therefore the path of oil and gas prices and the length of time for which they stay high. Secondly, investors should watch whether inflation starts to rise again, and whether central banks are forced to remain cautious for longer. Overall, the conflict reinforces our view of shifting traditional alliances, supply chain reallocation and diverging economic growth across regions. This mix is not neutral for markets and points to greater selectivity.

Key dates

Germany ZEW, US Retail Sales |

Korea GDP, Eurozone PMI |

Japan CPI, UK Retail Sales, Germany IFO |

Read more