Summary

Highlights

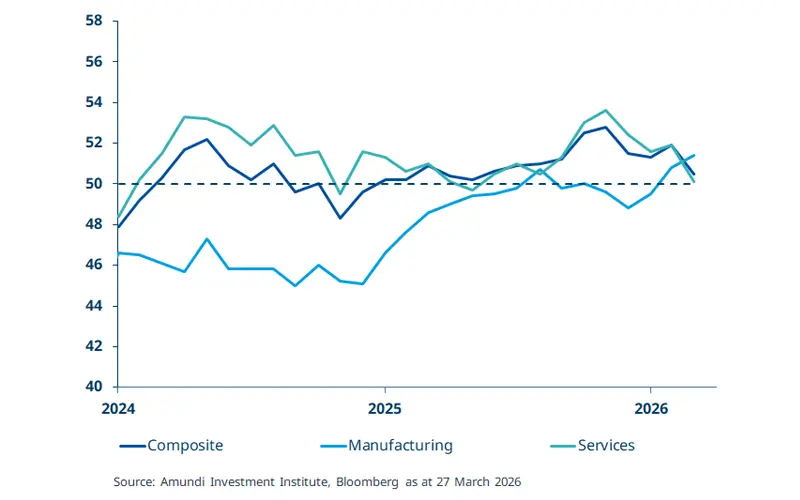

The Eurozone March PMI survey fell during the previous month, indicating businesses are getting worried about the Middle East conflict.

The composite PMI remained above the 50 expansion threshold, but it was the lowest in the past ten months.

Robust household savings, combined with new policy measures, should help cushion the economic impact across Europe.

In this edition

The preliminary composite Eurozone PMI (50.5) signalled a deceleration in economic activity in March. While the reading remains above the 50 threshold, it is the lowest since May 2025. Specifically, the manufacturing component rose, while the services component declined from February’s level. We believe businesses are pricing in some of the risks posed by the Middle East conflict: higher inflation, disrupted energy supplies and growth concerns. Looking ahead, we believe the crisis is likely to add stagflationary pressure to the economy through higher energy prices. If oil and gas prices remain elevated for a prolonged period, we may see inflation seep into other parts of the economy. As a result, the ECB’s task will become more complicated as the central bank tries to balance inflationary pressures with a nascent economic recovery. We expect the ECB to pause in the near term before making any further policy decisions.

Key dates

30 Mar Europe Confidence, India and South Korea Industrial Production, Brazil CPI |

31 Mar EA CPI, Japan CPI, US Consumer confidence, JOLTS data; China Manufacturing PMI |

3 Apr US Nonfarm Payrolls, Turkey CPI |

Read more