Amundi Client Servicing

Access your extranet (NAV, reporting...)

Thursday 03 October 2019

News, Fixed income

“Slowdown in global growth with subdued inflation and dovish Central Banks (CB) committed to avoid further economic deceleration are trends that should remain favourable for bond investors.” begins Eric Brard, Head of Fixed Income at Amundi. “On one side, investors should limit the upside in core bond yields and, on the other, support the credit market, despite the strong spread compression in this first part of the year. An increasingly selective approach will be crucial.”

A recent business intelligence analysis1 highlights that April 2019 was a turning point in bonds’ investments in both the USA and Europe. Total flows allow offsetting Q4 2018 in April and the market can expect positive flows afterwards. Passive funds are growing fast. Institutional investors seek again core strategies.

Other dominant forces within the fixed income environment are the increased role of politics, the still present short-term downside risks on the economy, the high level of debt globally and, moving towards the long-term, rising acknowledgment of climate and societal-related risks.

Against this backdrop, rethinking fixed income investments as a core part of investors’ portfolio is crucial both to deliver attractive risk / adjusted returns and to seek protection and effective diversification in the phases of market turmoil.

Amundi identifies three recurring themes for investors:

Considering the come back to potential GDP growth for most of developed economies, difficulties to achieve the inflation target for Central Banks and the high level of sovereign debts, which justifies also the vigilance of CBs, the current market equation is simple. Low interest rate + tight risk premia = high valuation. Clearly, active management, credit research and right solutions, particularly in terms of format positioning and access to the markets, are keys to cope with liquidity management and risk issues.

Traditionally, to increase their yield, investors have ended up taking additional liquidity risk (private debt, structured credit), duration risk (classic way to extend exposure at the far end of the curve with sovereign long-dated bonds) or default risk (high-yield). The market still presents some opportunities, either in sovereign or credit space. Indeed, within the defined low rates scenario unfolding on both sides of the Atlantic, the sub-segment becomes a key area to look at if properly screened.

Credit investment grade remains an attractive asset class for carry reasons, especially in Europe. Quality of corporate balance sheets were default rate is a lagging indicator, is a reality. Easy access to funding corporates is still true. These securities provide historical premiums over senior debt.

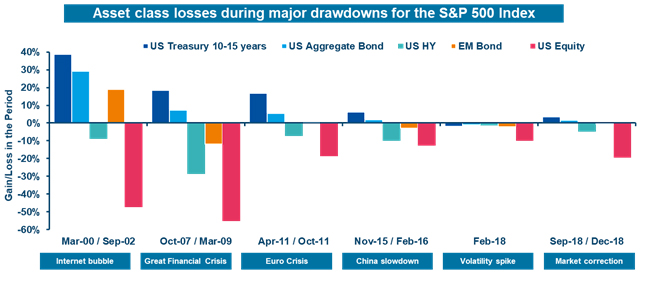

Government bond yields across the world are falling, as there is strong demand for safe assets and scarce supply. Investors in search for safe assets are looking at core bonds and high quality bonds as a diversifier of risk assets, during phases of market turmoil. As liquid assets, they will likely remain in strong demand.

Fixed Income are not only an alpha generator but also a potential shock absorber when market conditions are tougher on riskier assets. This year, the market story will thus be a carry and flexibility story.

Source: Bloomberg and Amundi, as of 13 June 2019

Fixed Income charts and views - July 2019

Revisiting fixed income opportunities after the European institution appointments

[1] Source: Bloomberg. Data as of 25 June 2019

Disclaimer: This document is not intended for citizens or residents of the United States of America or to any «U.S. Person» , as this term is defined in SEC Regulation S under the U.S. Securities Act of 1933. Amundi accepts no liability whatsoever, whether direct or indirect, that may arise from the use of information contained in this material. Amundi can in no way be held responsible for any decision or investment made on the basis of information contained in this material. The information contained in this document shall not be copied, reproduced, modified, translated or distributed without the prior written approval of Amundi, to any third person or entity in any country or jurisdiction which would subject Amundi or any of “the Funds”, to any registration requirements within these jurisdictions or where it might be considered as unlawful. Accordingly, this material is for distribution solely in jurisdictions where permitted and to persons who may receive it without breaching applicable legal or regulatory requirements. The information contained in this document is deemed accurate as at 31 August 2019. Data, opinions and estimates may be changed without notice. Document issued by Amundi Asset Management, a French “société par actions simplifiée”- SAS with capital of 1 086 262 605 euros - Portfolio Management Company approved by the AMF under number GP 04000036 —Registered office: 90 boulevard Pasteur — 75015 Paris — France — 437 574 452 RCS Paris - www.amundi.com

Policymakers continue to implement comprehensive strategies to fostering sustainable finance. Most notably, in March 2018, the European Commission adopted its action plan resting on three pillars: (i) re-orienting capital flows towards sustainable investments; (ii) managing financial risks stemming from climate change; and (iii) fostering transparency and long-termism in financial activities.

Moving towards 2020, volatility, agility and liquidity are the keywords for multi-asset investors: Accommodative central banks, economic slowdown and geopolitical hotspots will continue to move the market, offering opportunities.

The Democratic Party has announced the opening of an impeachment inquiry against President Donald Trump following revelations that he pushed Ukrainian President Volodymyr Zelenskiy to investigate the son of Democratic opponent Joe Biden. The impeachment process is long and articulated.