Listing your financial goals and when you want to achieve them such as short, medium and long-term is an effective way to get started. You should consider prioritising goals such as shelter, food, and safety.

Summary

Raising a family can often mean juggling many competing financial priorities. A goal-based approach can give each euro a job and will hopefully help reduce the load, freeing up time for other priorities.

Build a budget that supports your short-term needs and long-term dreams.

1. Start with your goals and timelines

2. Gather income and projected expenditure

In order to determine the exact amount of money that comes in and goes out it is a good idea to track everything by capturing combined monthly net income, fixed costs and variable or annual items.

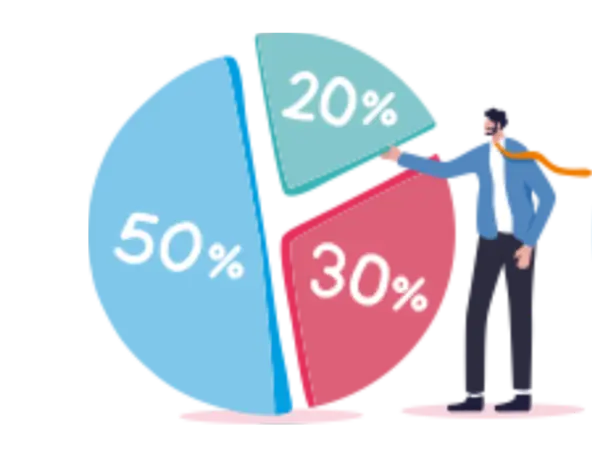

3. Build your family budget

Building an accurate family budget can take a lot of tweaking to get right. Every family is different so there is no formula to make it perfect. The good news is there are some general rules of thumb to help you get started.

Download the infographic to find out more about the 50,30, 20 rule.

4. Adjust where necessary

You should also consider adjusting your budget as circumstances change.

For example: new parents may see childcare and essentials take 50-65% of income - try to keep contributing to retirement and maintain a 3–6 month cash cushion; parents of school-age children can redirect lower childcare costs into education and retirement savings; and those nearing retirement or with an empty nest may wish to increase retirement contributions and mortgage repayments.

5. Protect today. Secure tomorrow

Consider appropriate insurance or other risk protection to safeguard household income and your financial goals. You may also want to ensure your estate basics such as wills, beneficiary designations and powers of attorney are up to date. You might not feel it’s important right now, but it can be essential even for young families.

6. Monitor, review and adjust!

Review your budget monthly at first, then when you have found what works for you, you can check it less frequently. You can also reallocate expenses as life changes - new child, job change, move, education bills, caregiving.

There are tools available to guide you such as budgeting apps and spreadsheets and as a final tip, check employer benefits and parental leave entitlements which may reduce out of pocket costs.

Download the guide

Discover more

Prepare for your retirement dreams

Set it and forget it: investing made easy at any age

Pensions for women: Taking control of your financial future

Your 7-step roadmap to investing for your retirement

Wondering where to go for help?

You have the choice when it comes to the “where”. Our range of funds are available from your local bank, broker or financial advisor.

|

|

|

Contact your | Contact your | Contact your |

Unless otherwise stated, all information contained in this document is from Amundi Asset Management S.A.S. and is as of 19 March 2026. Diversification does not guarantee a profit or protect against a loss. The views expressed regarding market and economic trends are those of the author and not necessarily Amundi Asset Management S.A.S. and are subject to change at any time based on market and other conditions, and there can be no assurance that countries, markets or sectors will perform as expected. These views should not be relied upon as investment advice, a security recommendation, or as an indication of trading for any Amundi product. This material does not constitute an offer or solicitation to buy or sell any security, fund units or services. Investment involves risks, including market, political, liquidity and currency risks. Past performance is not a guarantee or indicative of future results.

Date of first use: 19 March 2026

Doc ID: 5144006